Robo-Advisor Portfolio Optimization

Automated Portfolio Recommendations with Utility Maximization • Arp 2025 - May 2025

Project Overview

This project develops a comprehensive Robo-Advisor demo that helps users generate optimized stock portfolios based on their risk preferences and return targets. The system simulates traditional utility-maximization strategies and implements a front-end tool that visualizes optimized portfolios and performance metrics.

Introduction and Objectives

The Robo-Advisor module aims to automate personalized portfolio recommendations using conventional investment principles:

- Utility Maximization - Simulates investor preferences using a utility function based on risk and return

- Mean-Variance Optimization (MVO) - Constructs portfolios to maximize expected utility

- User Personalization - Supports varying risk preferences and return targets via a web interface

The final system demonstrates how technical parameter choices and behavioral biases can impact investment outcomes.

Methodology

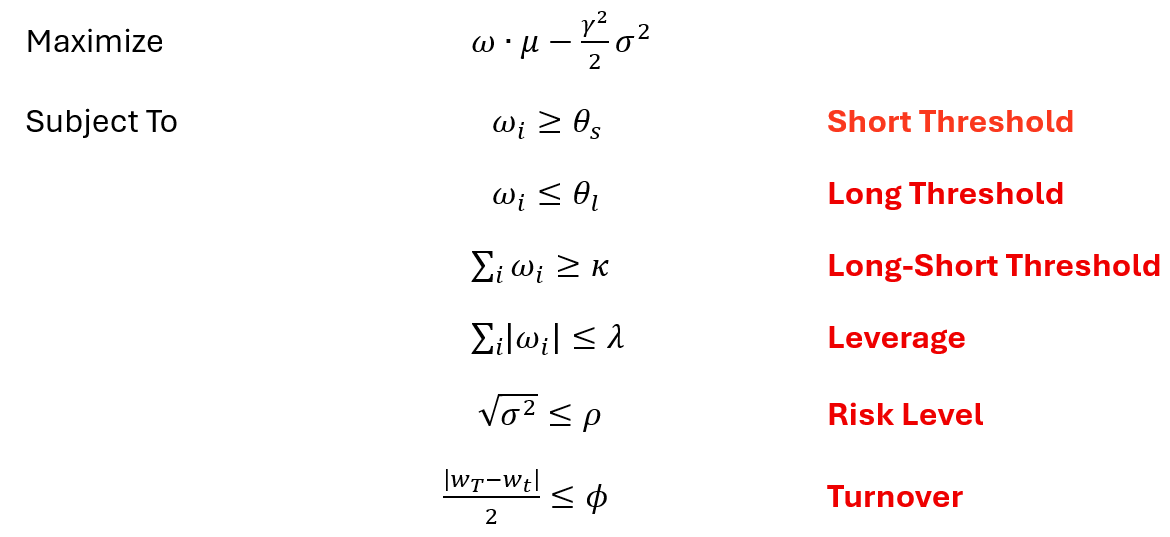

1. Utility-Based Portfolio Construction & Configuration

We model the investor's objective using a utility function for portfolio optimization:

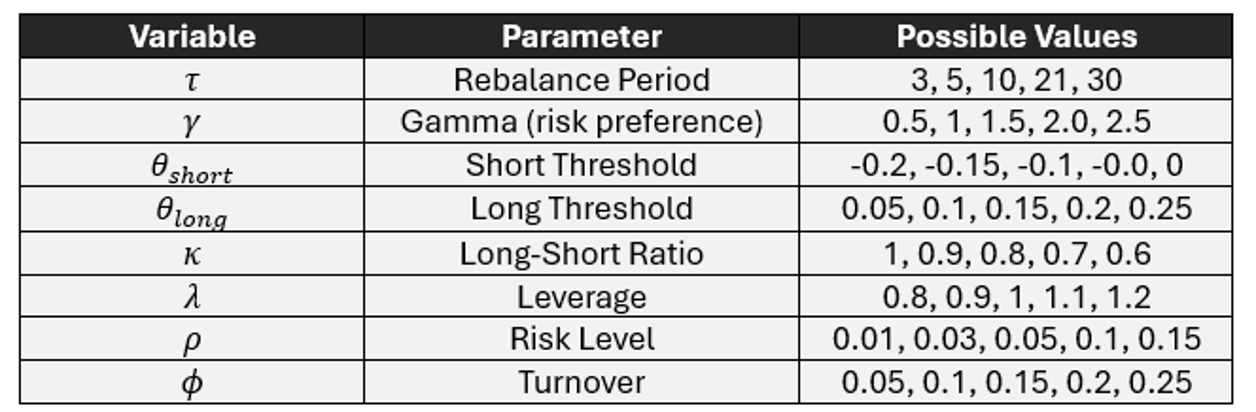

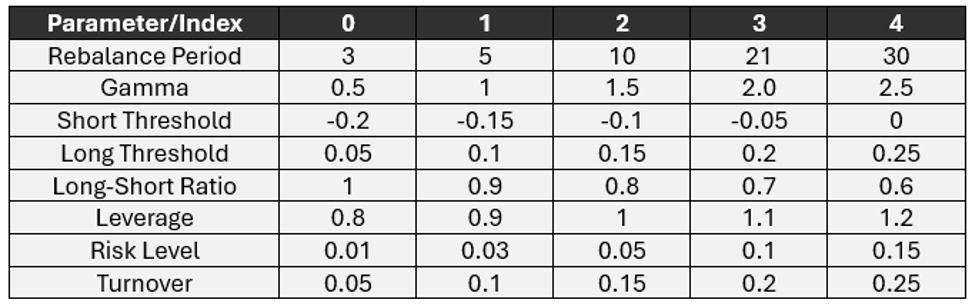

Various combinations of technical parameters are tested to simulate portfolio configurations:

A scatter plot shows the top 100 performers out of 5,000 sampled portfolios, with comparisons to the S&P 500 and equal-weighted portfolios based on Sharpe ratio. For detailed results and analysis, please refer to the IEDA4500 Final Report.

2. User Behavior Simulation & Assessment

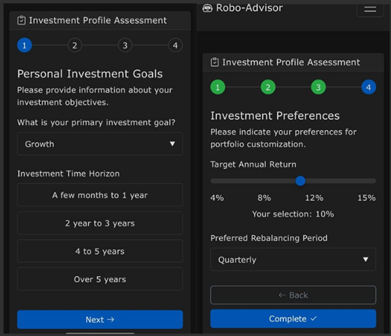

To bridge the gap between technical parameters and user-friendly interactions, a comprehensive questionnaire was designed. The assessment covers:

- Personal Investment Goals - Growth strategy and time horizon

- Risk Tolerance - Comfort level with market fluctuations (conservative to aggressive)

- Financial Situation - Saving habits, cash flow, and capital base

- Investment Preferences - Target return, rebalance period, and diversification

A parameter index table is initialized using technical parameters, with user responses mapped to derive portfolio configurations:

The detailed mapping rules can be found in the IEDA4500 Final Report.

3. App Demonstration

New users complete an intuitive questionnaire to initialize technical parameters:

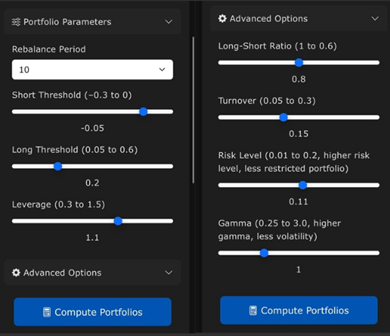

Users can fine-tune settings based on their investment insights:

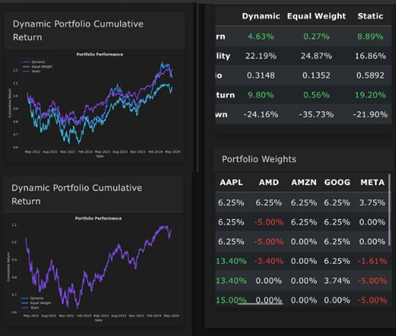

Portfolio performance is visualized across rebalance periods:

Technology Stack

Limitations and Potential Improvements

- Sensitivity Analysis - More systematic evaluation of how each parameter impacts performance is needed

- Adaptive Tuning - Use of heuristics or advanced optimization (e.g., evolutionary algorithms) could improve portfolio quality

- Data Expansion - The current stock universe is limited. Including more assets or asset classes would improve real-world realism

Repository

Find the source code and report:

View Repository on GitHubLicense

This project is open-source and available under the MIT License.